Class is in session!

Find a comfy spot, get your thinking caps out, and brace yourselves for some seriously satisfying graphs. Why, you ask? Well, this month’s IG live session was packed to the brim with all the juicy details you need about the current and future real estate market landscape.

We’ve seen some MAJOR shifts in recent years — both socially and economically. The real estate market evolved drastically since the peak of COVID. Whether you’re looking to buy or sell a home, I understand how tough it can be to sift through the doom and gloom of market reports, and figure out what’s really going on so you can make those crucial decisions.

I’VE GOT YOUR BACK

That’s precisely why I’m stoked to bring in the experts for some real talk on my IG. We’re here to tackle those burning questions head-on and get you answers from people who know their stuff.

Join me and the fantastic Julee Felsman (@workshopmortgage) as we explore interest rates, historical data, economics, and housing forecasts. Geek out with us!

If you’re new here, I’m Lauren Goché — a Portland realtor with a decade of experience backing me up. Which means I’ve weathered more than a few market shifts over the course of my career, and specialize in making sure you can make the most of the market for your goals. Read more about me here.

Meet Julee Felsman

She’s not just your run-of-the-mill mortgage broker — oh no, my pal Julee is a bonafide mortgage legend with an impressive 29 years in the game.

Julee lives and breathes data. For a living, she dives into the nitty-gritty and breaks it down for those of us who aren’t mortgage lending aficionados. I highly recommend checking out her YouTube channel where she chats about home buying, mortgages, real estate investing, and other related topics, in a digestible way.

Now, beyond the mortgage realm, Julee leads quite the life with her spouse and way too many I mean, the PERFECT amount of pets 😉 😻

You can find Julee over at Guaranteed Rate (NMLS #120831), where she’s happy to chat about any of your mortgage lending needs. You’re in good hands with this mortgage maven!

Let’s Take a Deep Dive into Interest Rates

The not-so-great news:

Interest rates have taken a bit of a hit over the past few months. A mix of factors has come together, putting pressure on the Fed to consider raising rates. Let’s hear from Julee on this:

“Some of it’s real and some of it I would say is a little bit of a construct. The Fed has been raising interest rates with the goal of slaying the inflation dragon — and they probably have. But if they say it out loud, then people will start spending and borrowing money again, which are behaviors that lead to inflation… And that could reanimate the dragon.”

What’s on the horizon? The Fed will keep up their “tough talk” to maintain control on inflation. We’re not quite out of the choppy waters just yet!

The good news:

Here’s Julee’s reading on things:

“The inflation Dragon is slain, but the Fed won’t admit it just yet. The other good news is somehow — and I would have bet my money otherwise — the Fed pulled it off without creating a recession. I don’t think that’s coming.”

Are We in a Recession or a Vibecession?

The one piece of data keeping economists from saying we’re in a recession is that the job market is strong. But you might be saying to yourself “Lauren, that just doesn’t feel right because everyone I know is being affected by layoffs…” — And I’m there with ya. The data is not matching our lived experiences, so what gives?

Now, Julee introduced me to a term and I’m allll about it — ‘vibecession’ — doesn’t it just hit the right note? The data is saying we are definitely not in a recession. But the vibeeeeee??? I think we, and our pockets, can all agree the vibe is giving recession.

Yet the economic data is surprisingly holding up.

Here’s a direct quote from Kyla Scanlon, the person who coined the term:

“People want a simple solution for Why Things are Bad (and I do too) but things are bad (and good) for many different reasons. The overwhelming nature of it all creates a Vibecession. Where economically speaking, things are okay-ish but in reality… the vibes are off. People are feeling bad.

Vibecession – a period of temporary vibe decline where economic data such as trade and industrial activity are relatively okayish”

Feel free to get a full breakdown of vibescession here.

Here’s the takeaway from all of this: If you find yourself slipping into a doomsday mindset, just know that things will be alright AND we’ve got the data to back it up.

More good news…

Let’s quickly jump back to the topic of layoffs, because Julee had an eye-opening tangent worth thinking about:

“Layoffs are hitting pretty close to home, especially here in the Portland market. Interestingly, a lot of these job cuts are hitting the tech sector, which is a big part of the Portland scene.A few large companies have been hoarding all the really smart, talented, tech-savvy people — you know, Google, Apple, Facebook and so on. Some of those companies are pulling back from the massive hiring spree they went on during Covid. Now, that talent pool can disperse into other industries and we’re gonna see bursts of wonderful productivity. The coders, the designers, the programmers, and all the brilliant people who know how to make the magic happen, can you come to impact my industry and your industry and all the others.”

Now holy shit, that’s REAL.

Why You Should NOT Wait for Prices to Drop

Julee and I had a candid chat about this, and we’re on the same page. A lot of people are waiting for prices to come crashing down before they buy a home. And the reality is — that happened already.

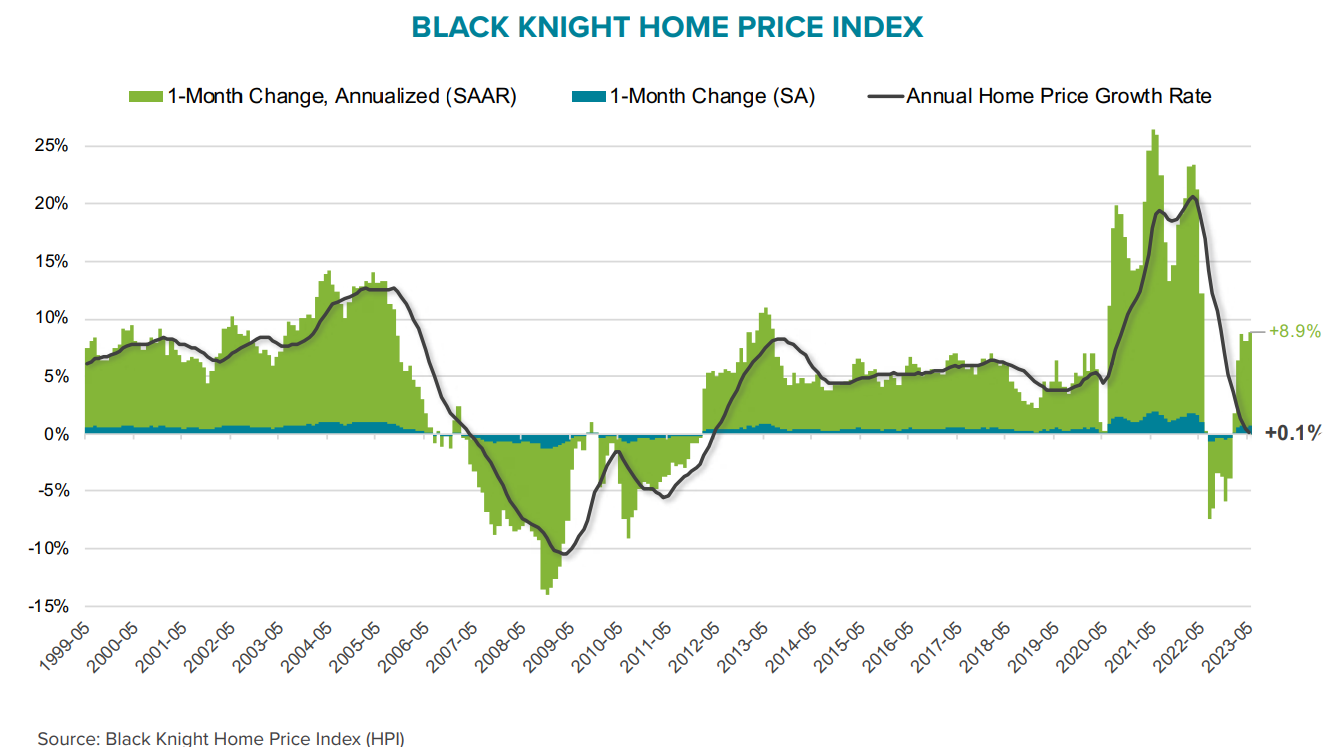

Let’s pull out the graphs! There’s the crash… see it? The little dip up on the upper right. That ship has sailed and we’re on our way back up.

Here’s another graph showing the Home Price Index and here’s what the data concludes: “If recent trends hold true, that annual home price growth rate would remain at or near 0% for a very small handful of months before trending sharply higher“

And if you’re not already convinced, we’re up a lot month over month in Portland:

Why won’t prices drop? — We still have an inventory problem

This is Economics 101: To bring prices down, we need an increase in supply OR a decrease in demand. The Fed lowered demand by keeping interest rates high — essentially pricing out millions of people from buying a home.

But despite that, there are still more people looking to buy homes than there are homes on the market. And let me tell you — I hate it. The truth is affordability is slipping more and more out of reach, and it’s the folks on the edge of homeownership that get hit the hardest.

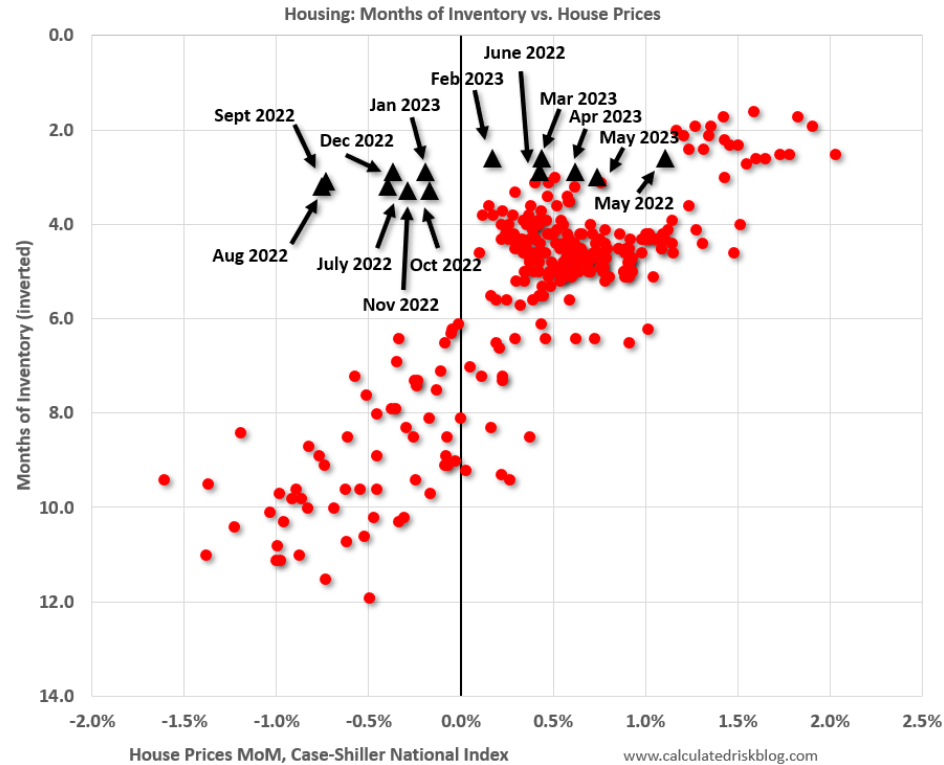

Here’s a graph on the relationship between housing prices and inventory — as inventory goes down, prices go up. The black triangles are recent data points and the red dots are historical data points. Do you see how unusual last year was?

Once rates go down, the market will flood with buyers

For you sellers, this is fantastic news, but for potential buyers, not so much. The moment interest rates go down, a surge of fresh homebuyers will pour in, amplifying competition and driving home prices up.

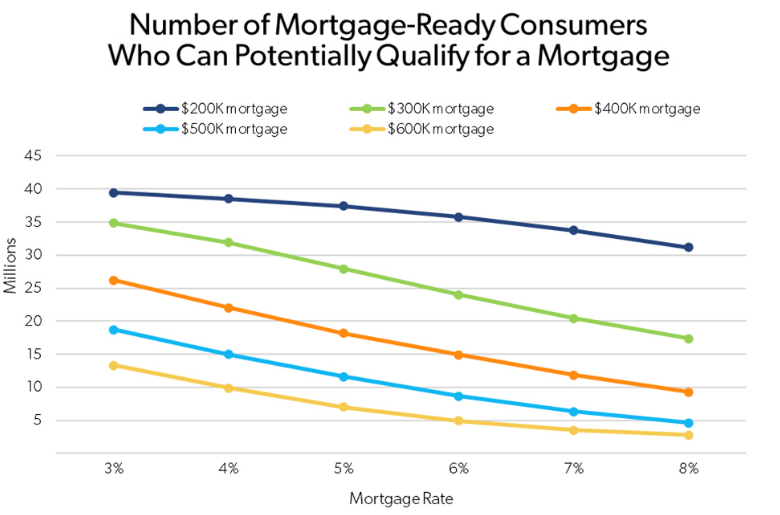

Freddie Mac, one of the major players in mortgage purchases, did a study on the impact of interest rates on what they call “mortgage ready homebuyers”. They found that every time rates rose 1%, we lost nationally, 3 to 4 million people out of the pool of mortgage ready homebuyers. And you know who gets hit the hardest? It’s those folks who were just trying to get their foot in the door at the lowest price points.

When interest rates eventually make their way back down (which according to Julee could be very soon) we can expect a wave of homebuyers rushing into the market.

So what will fix the housing inventory problem? Julee and I dug into this a bit, and I’ll be honest, we’re still piecing together where all the inventory will come from. The cold, hard truth is: we’re just not building enough houses, and we might not ever catch up with inventory.

We even entertained some pretty wild thoughts. Like, imagine if we cracked the code on an affordable way to 3D print houses — but hold on a sec, we’re not quite in the future yet, are we?

We tossed around a bunch of ideas:

- Boomers Riding into the Sunset: Could the inventory shortage smooth out as the boomer generation naturally transitions? — Julee says we won’t see the full effects until another decade rolls by.

- ADUs to the Rescue: Yup, Accessory Dwelling Units might be part of the solution. Gotta love a good ADU, right?

- And then there’s sticking it to capitalism and teaming up with your bestie to snag a duplex or other cohousing solutions. More on that this fall with @ridefreefearlessmoney — Keep your eyes peeled!

The tech might not be quite ready for house-printing magic, but Julee and I are keeping our eyes peeled for the next big thing in the world of housing inventory.

Autumn Interest Rate Projections

Let’s first chat about expectations: A sweet spot for a healthy interest rate is in the 5s. Back when rates were dancing in the 2s and 3s, things weren’t exactly rosy. So, let’s not hope for or anticipate rates diving back to those levels.

Now, let’s delve into predictions. Julee anticipates that interest rates will stabilize around 5% within the next 18 months, give or take six months — and her hunch leans more toward the lower end of that range.

She has three solid reasons to back this hunch up. Let’s get into the nitty-gritty:

- 10-Year T Bill and Mortgage Rates Gap: Think of the 10-year T bill as the bellwether for 30-year mortgage rates. Lately, the gap between them has been much bigger than usual, even reaching 3% at times — normally, it’s around 1.5% to 2%. When the reasons for this gap go away and it starts to close, we could see a drop of about 1% to 1.5% in mortgage rates. This won’t happen overnight, but it’s on the Fed’s radar.

- The CPI data is lagging: The Consumer Price Index is the first meaningful read on inflation we get every month. Almost half of CPI is tied to housing, but here’s the catch: measuring housing is slow — The Bureau of Labor Statistics has to call people one-by-by to find out rent prices. Now, the CPI has been getting closer to the Fed’s target of 2% and since housing data is slow, we might have already reached that target without knowing it.

- Geopolitical Factors: The ongoing war in Ukraine hasn’t been good for the economy. But what’s bad for the economy often translates to good news for rates.

Wrapping Things up…

What Aspiring Home Buyers Should Know:

- Keep in mind, prices probably won’t drop further – that dip already had its moment.

- Buy ugly, sell cute. Don’t shy away from homes with a bit of ‘character’ — they often come at a discounted rate compared to the more “cute” ones.

- High interest rates CAN be your friend – They help keep the competition in check and the home prices steady.

- Once rates go down, the market is going to get flooded with buyers. Our advice: Get a house while it’s not as competitive, and then refinance later — Plus, you most likely won’t pay lender fees. More on that in my blog here.

- Back in the day, selling a house within 2-3 years could still bring in profits. Nowadays, it might take a bit more time, but trust us, in the long haul, you’re likely to see gains. There hasn’t been a single moment where homes lost value after a 10-year span.

What Sellers Should Keep in Mind:

- Houses that are priced, prepped, and marketed poorly are sitting on the market. Houses that are priced well, prepped well, and marketed well are still getting multiple offers.

- During the selling process, even if you have multiple offers, it’s important to be mentally prepared for the inspection phase. In this market, sellers have more power to negotiate, so expect having to get some repairs done in order to seal the deal.

- Oh, and by the way, *CUTE* is the magic word – take a peek at my staging blogs to see what I mean.

As always, I’m here to help you navigate the real estate waters. Whether you’re looking to buy, sell, or just have some real estate questions, feel free to get in touch with me here.